")

One of the things most Filipinos struggled with is having easy access to different kinds of financial services. Not everyone has bank accounts or investments because it’s just hard for some to create accounts.

Reasons can be because banks are just far or maybe there are long lines that we can’t afford to take because we have things to do or it’s open only on weekdays and you’re at work during business hours.

Sometimes it can be because of the requirements which usually is 2 valid IDs and you just have one.

But thanks to the growing financial systems, there are now few ways to create bank accounts just using our phones like what I’ve shared with you in the past about UnionBank.

Unionbank is great so far but there are also a few downsides like having an annual fee and no interest on deposits. So I personally don’t store my money there.

I mainly use it for receiving my paycheck from my online work. Do InstaPay transfers (which is up until today is free) and making online card transactions. But after that my balance is all transferred to GCash to put it in GSave or GInvest.

Nothing is actually bad with what I’m currently using but a buzz is going around for this new app called Tonik. So I’ll review it before you even try it.

How to Open a Personal Bank Account Using Unionbank’s Mobile App

What is Tonik Bank?

Tonik Bank is a neobank which means they are branchless and operates fully online. Because they are branchless, it means less cost for them that’s why they are able to provide higher rates for their depositors.

It’s easy to use and has a lot of interesting features which you’ll find out more about today. Also, they are licensed with BSP, and deposits are insured by PDIC (500k deposit insurance in PH) which are all common with all known banks. So to cut it short it is a legit bank. But there’s a lot more to cover, like what are those interesting features and whether it’s advisable to use them or not.

What are the interesting features of the Tonik App?

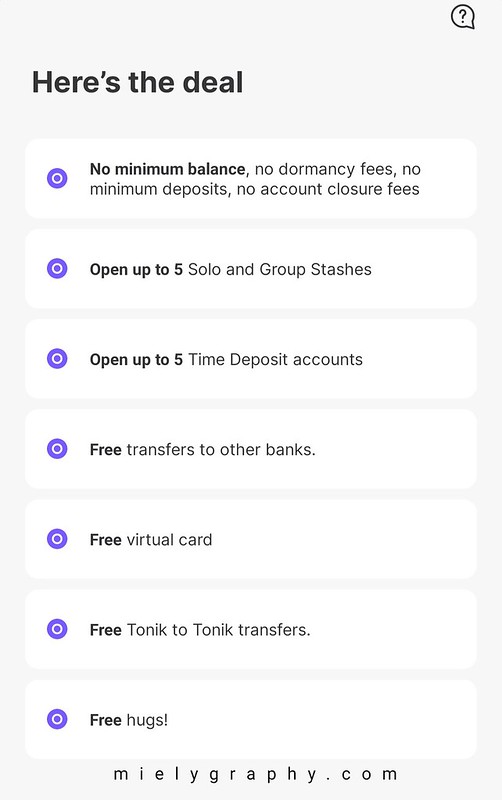

First of all, they claim what all of the new digital banks have like: No maintaining balance required, free transfers free almost anything, easy process and all that kind of stuff. Well, when GCash started to become serious about the mobile wallet services they’ve done that too to attract users. But after it has become popular they started to add fees in almost any of the transactions you can do with it.

We’ll check on that later on with Tonik but here are the financial products Tonik has that make it very unique.

Savings account with Tonik

So the standard savings account is the first thing you’ll see in the Tonik app once you’ve registered and here’s where all your cash-ins will go.

They offer 1% interest here.

This is the main account, so your balance must be in this part if you have to transfer money to other people.

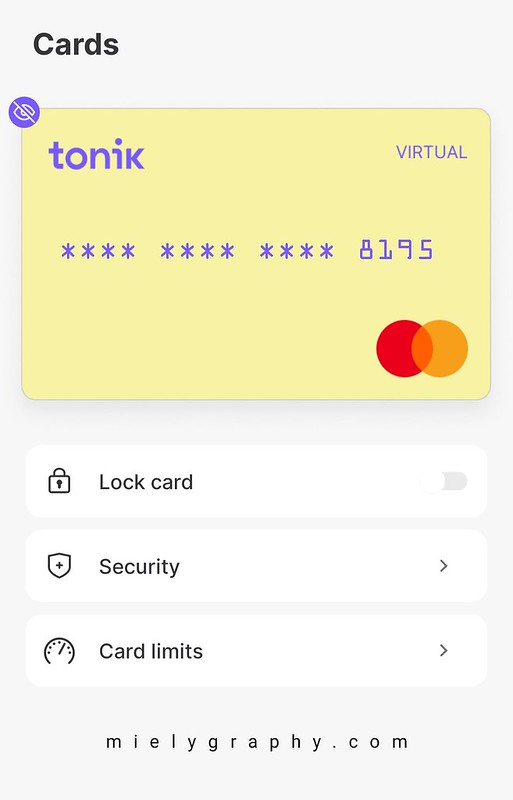

Virtual Master Card

I like this feature, because from registration and being verified you’ll already have a virtual card that you can use for your online transaction.

The good thing about it is that first of all it’s a master card unlike with what I’ve used with GCash it’s AMEX virtual card which is not always accepted and for some reasons GCash keeps on failing transactions with it so I don’t use it anymore.

Also, with their virtual card, you can enable it or disable it any time to avoid accidentally renewing your free trials or subscription renewals. I love it because I can use it in the play store without worrying about my kids making accidental purchases.

You also have the option here to change the maximum transaction limits just in case you want to control your online spending or just trying to keep safe of your balance in case your virtual card details have been compromised.

They claim to have a physical debit card on their site and they even discuss the fees for ordering one but on the app, I see that it’s still coming soon.

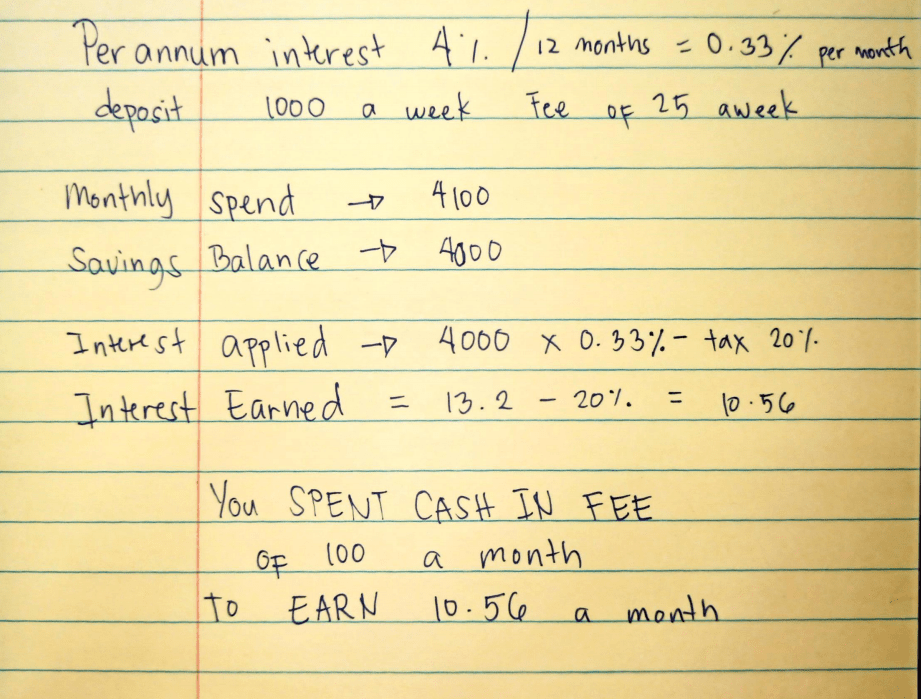

Stashes

If you’ve seen my old post about UnionBank Goals it’s similar to that. You can set a goal or just a separate place where you can create an account for a specific purpose. It offers a higher interest rate than your regular account which is 4%.

They also have a group stash where you can collaborate with another Tonik member(s) to fund it and that gives a 4.5% interest rate. I haven’t tried the group stash but according to Tonik’s website, only the group stash creator will be able to withdraw funds.

There’s also a catch on the group stash interest rate. You’ll only eligible for 4.5% if the group stash consists of you and another 2 members.

But don’t worry if you’re stashing with a group, they do have a transfer feature for Tonik to Tonik users and it’s also free of charge.

Kick Start Your Goals with UnionBank App

Time deposit

Yes finally! They have time deposits with a higher rate of up to 6% and you can start with a minimum deposit of 5000 PHP and you can leave it there from a minimum of 6 months up to 24 months.

I just find it weird because the highest rate goes to the shortest term which is 6 months.

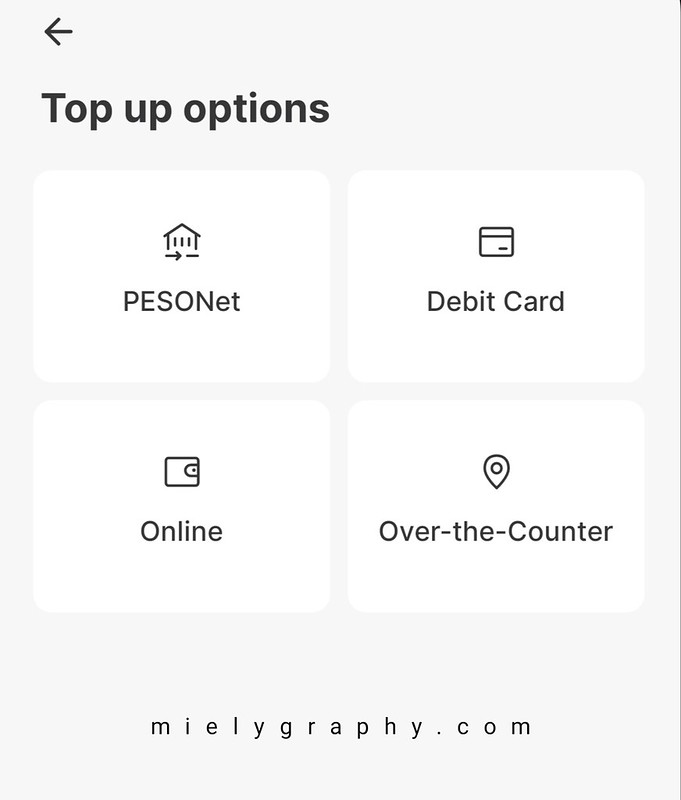

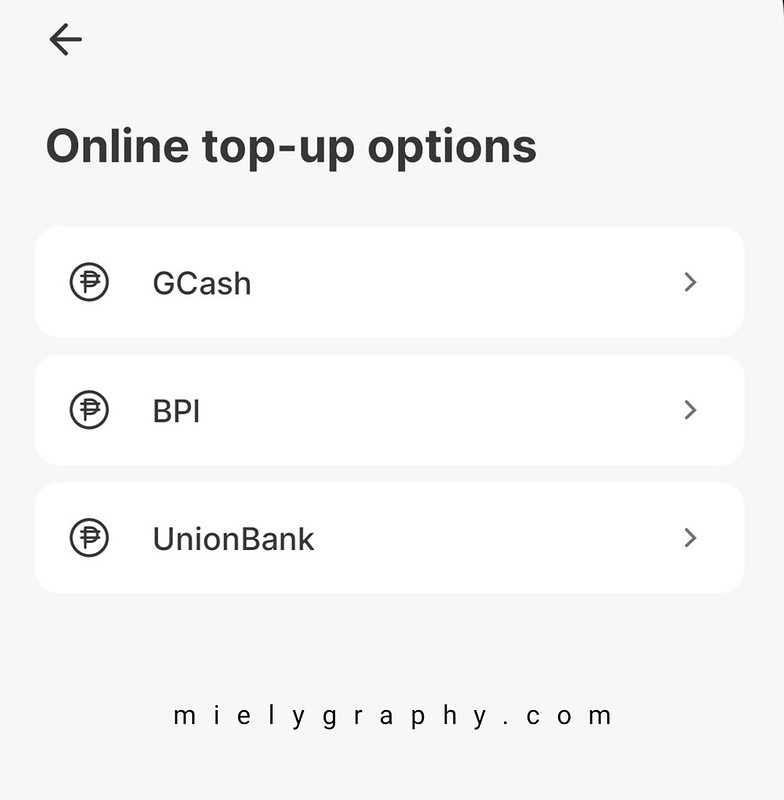

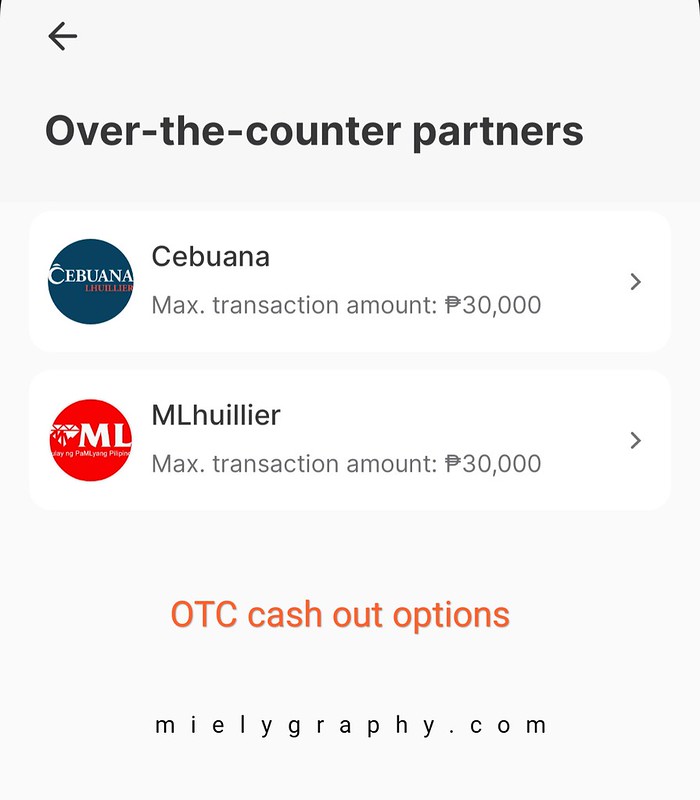

Cash In and Out Options

At this point all cash-in and cash-out options are free except some of the over-the-counter options. You can refer to this site for the fees.

For cash-ins you can use the following options:

- PESONET

- ONLINE (GCASH, BPI AND UNIONBANK)

- DEBIT CARD

- OVER-THE-COUNTER

Here are the Cash-Out Options

- InstaPay Bank Transfer

- GCASH

- To Other Tonik Users (using phone or account number)

- Over-the-counter

InstaPay Bank Transfers

Let’s talk about the pros of Tonik Bank

Well yeah, we’ve discussed so far the high rates of their savings products and the interesting products they currently offer. But is there something else for the pros?

Yeah, I think the app itself is really nice. Among all any other banking apps this one is the most user-friendly.

Also if you’re in a rush to create an account and you don’t have your ID at the moment they have an option to skip the ID verification. By doing that your account may be limited. If you don’t get verified your account will only be valid within 12 months with 50K deposit limits and 2 stashes.

Anyway, it’s just good to know in case someone is sending you through Tonik and you’re commuting and needing to create an instant account. LOL.

Cons of Tonik App

I don’t wanna break it with you now but I have to let you know. Let’s start with the mildest to wildest cons. 😅

- The app has the option to view your transaction history but it doesn’t have options to filter and no option to generate statements. I don’t know why some financial apps missed that but I think it’s important because statements can be used as validating documents.

- Lack of bill payments. What kind of bank doesn’t have that? Please let me know. Hahaha.

- Their stash is not perfect too. I think it would’ve been better if they have like an auto transfer to stash. GSave and Unionbank have that kind of feature for auto transfer so why not?

- The killer con, starting July 5, 2021, they’ll start collecting 25 PHP FEE for cash in transactions from most channels (booooo). I think they’ll have free cash-ins with PESOnet but who uses PESOnet? Hahaha, that’s the slowest form of online transaction that I don’t understand why ever existed. LOL.

3 thoughts on “Tonik Bank Review – New Neobank in the Philippines?”

Hi! I just want to know what similar banks have no cash in fees like you mentioned towards the end of your post. Hope you could also make an article about that. Very helpful post! Thank you! ♥️

Thank you Kamylla… So far I’ve used Unionbank and GSave (Cimb)… Usually cash in fees applies to GCash only…and for most banks they use transfer fees. I think it’s fair enough to have fees but then the amount is to big and PesoNet also has charge.

I usually deposit on my tonik using unionbank online direct since that method has no fees. You can also try BPI as they now have online registration most of their branches has deposit machine. BPI is also included on Tonik’s free cash in method using bpi direct online.

I just really feel sad about GCash method for having fees because most GCash users also pays cash in fees and it will be doubled if they have fees on gcash and tonik.. but overall Tonik’s offers are great.